If my foresight were as clear as my hindsight, I should be better off by a damned sight.

If my foresight were as clear as my hindsight, I should be better off by a damned sight.

IBM Acquisitions by CEO: 2001 through 2023

|

|

Date Published: July 28, 2021

Date Modified: March 16, 2024 |

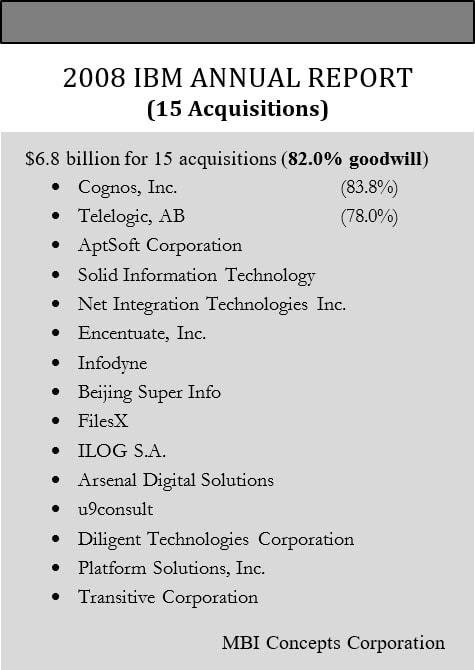

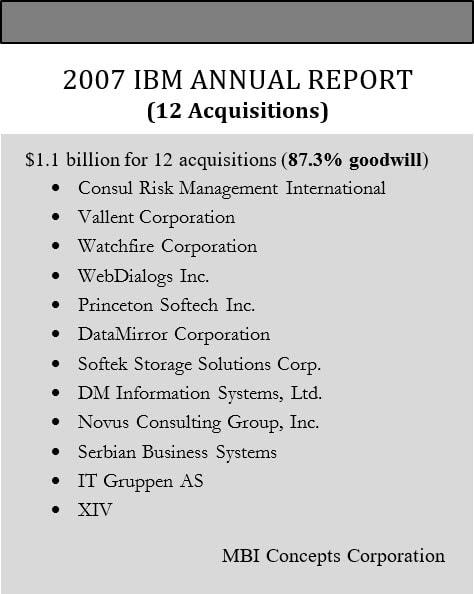

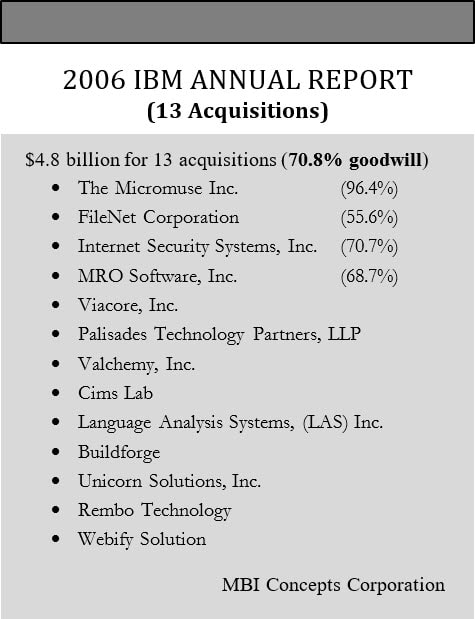

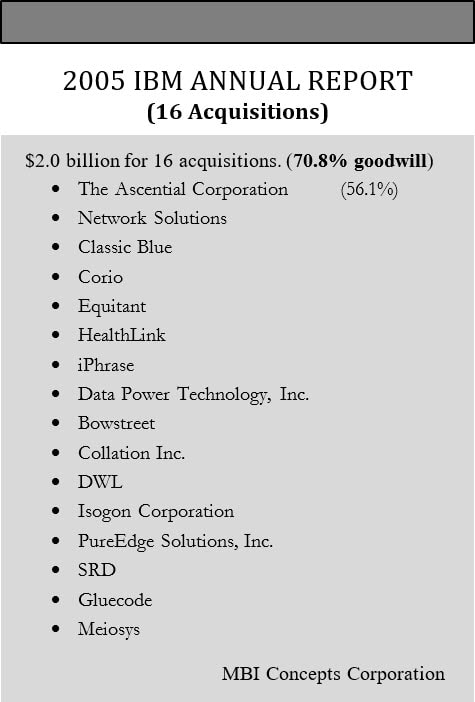

"SFAS No. 142 eliminates the amortization of goodwill, requires annual impairment testing of goodwill and introduces the concept of indefinite life intangible assets. It was adopted on January 1, 2002. The new rules also prohibit the amortization of goodwill associated with business combinations that close after June 30, 2001."

IBM 2001 Annual Report

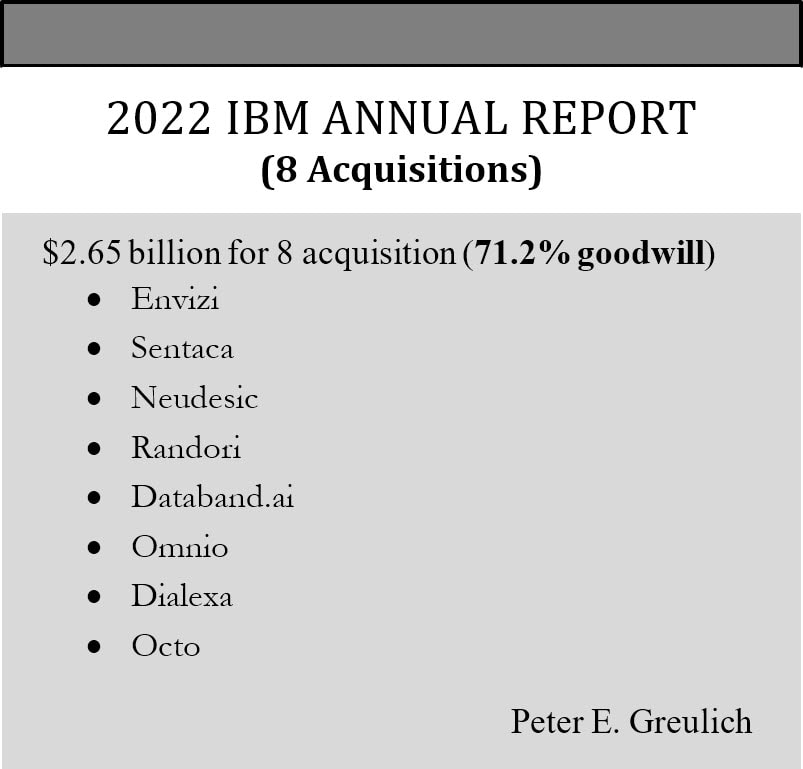

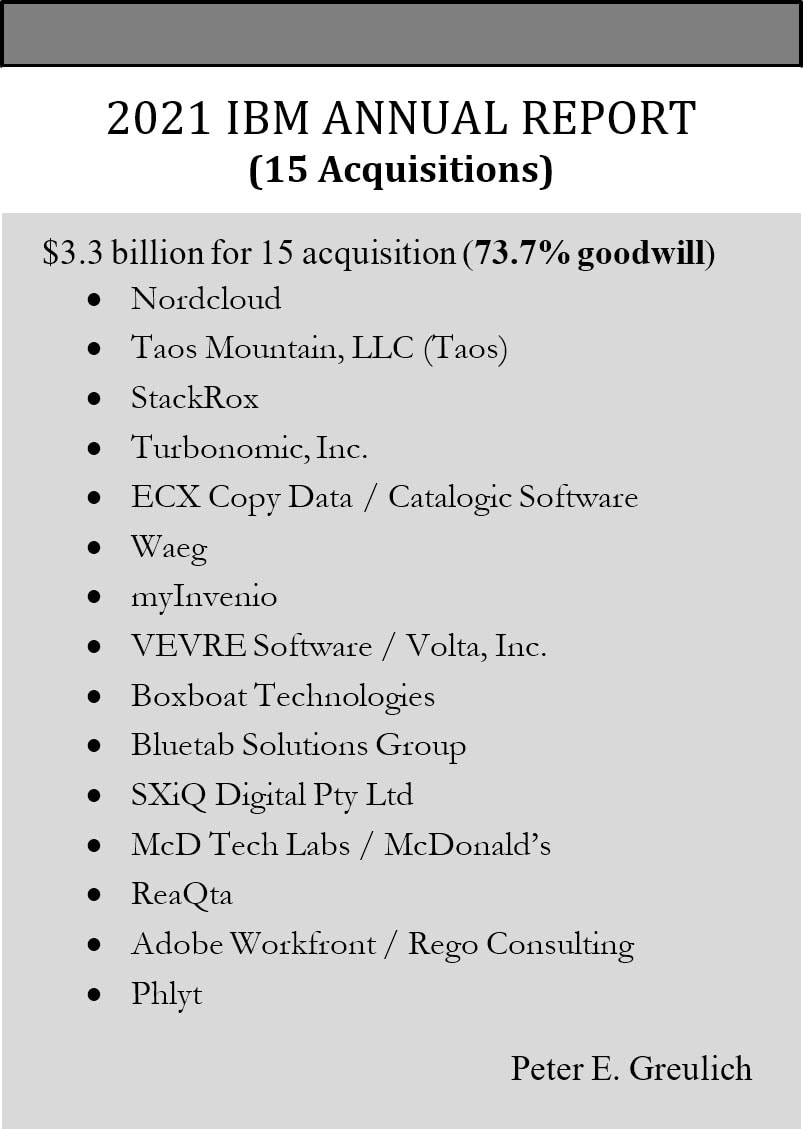

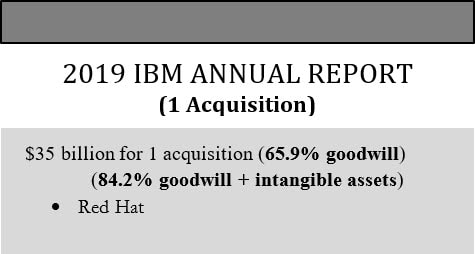

To understand how IBM's usage of a 2001 goodwill accounting change for its 224 acquisitions (2001-2023) listed here at a total cost of $100 billion has been increasing shareholder risk read this article: [Shareholder Risk]

|

Arvind Krishna's

Acquisitions Total Acquisitions: 39 acquisitions Total Outlay: $11.9 Billion List of Acquisitions: 2020 to 2023

|

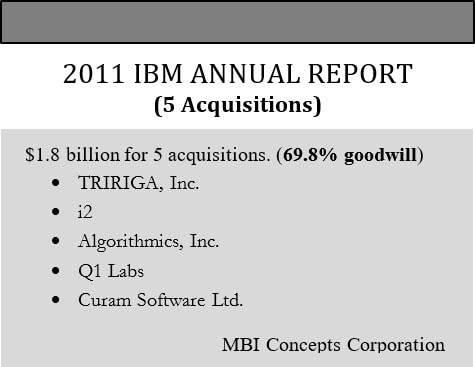

Virginia M. Rometty’s Acquisitions

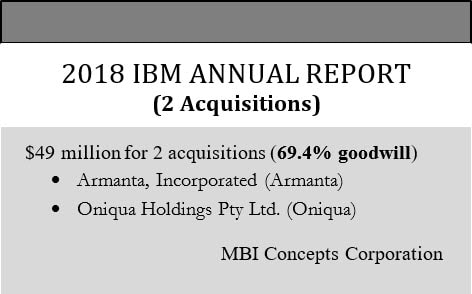

Total Acquisitions: 64 acquisitions Total Outlay: $52.5 Billion List of Acquisitions: 2012 to 2019

|

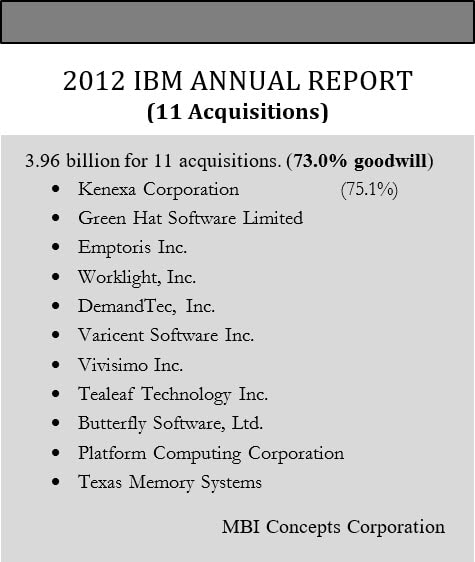

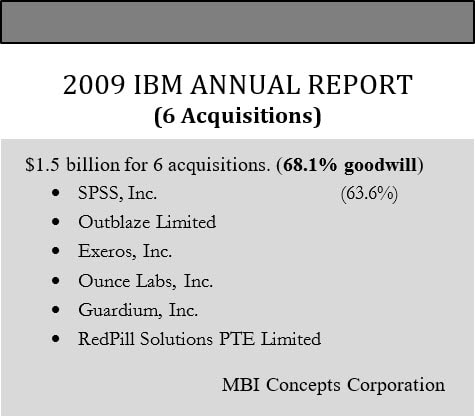

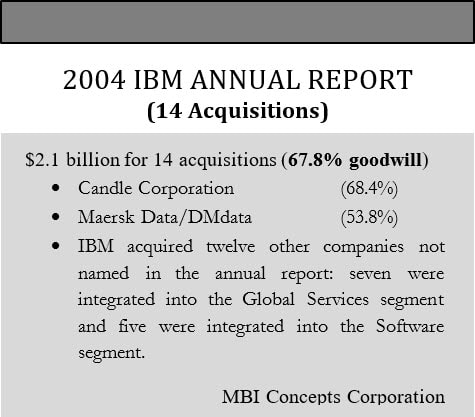

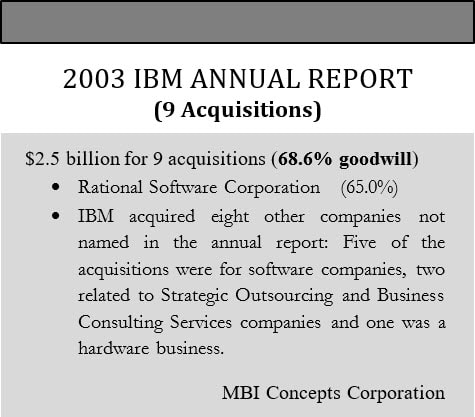

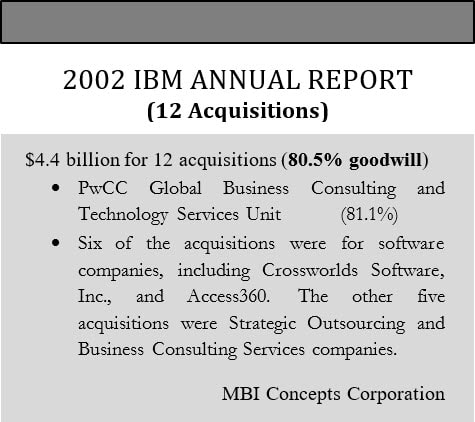

Samuel J. Palmisano’s Acquisitions

Total Acquisitions: 119 Acquisitions Total Outlay: $33.7 Billion List of Acquisitions: 2002 to 2011

|

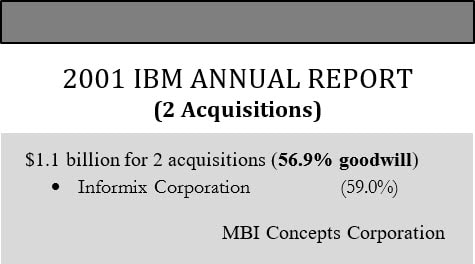

Louis V. Gerstner’s Acquisitions

Total Acquisitions: 2 Acquisitions Total Outlay: $1.1 Billion List of Acquisitions: 2001

|