If my foresight were as clear as my hindsight, I should be better off by a damned sight.

If my foresight were as clear as my hindsight, I should be better off by a damned sight.

Learning from Mistakes: Warren Buffett and IBM

|

|

Date Published: July 31, 2021

Date Modified: June 30, 2024 |

What Warren Buffett Needs to Learn from His IBM Investment Mistake

- Warren Buffett’s Philosophy of Castle Walls and Enduring Moats

- IBM Was More than Brick and Mortar, and Deep Ditches Filled with Water

- IBM Needs to Inspire Enthusiasm, Engagement and Passion in its Stakeholders

Warren Buffett’s Philosophy of Castle Walls and Enduring Moats

A truly great business must have an enduring ‘moat’ that protects excellent returns on invested capital. The dynamics of capitalism guarantee that competitors will repeatedly assault any business ‘castle’ that is earning high returns. Therefore, a formidable barrier such as a company’s being the low-cost producer—or possessing a powerful world-wide brand—is essential for sustained success.

Warren E. Buffett, Letter to the Shareholders of Berkshire Hathaway, Inc.

Why did Warren Buffet invest in IBM? He told CNBC's Squawk Box that he had been "hit between the eyes" by how IBM found and kept its clients. He believed he had found an "enduring moat" at IBM: its customer loyalty.

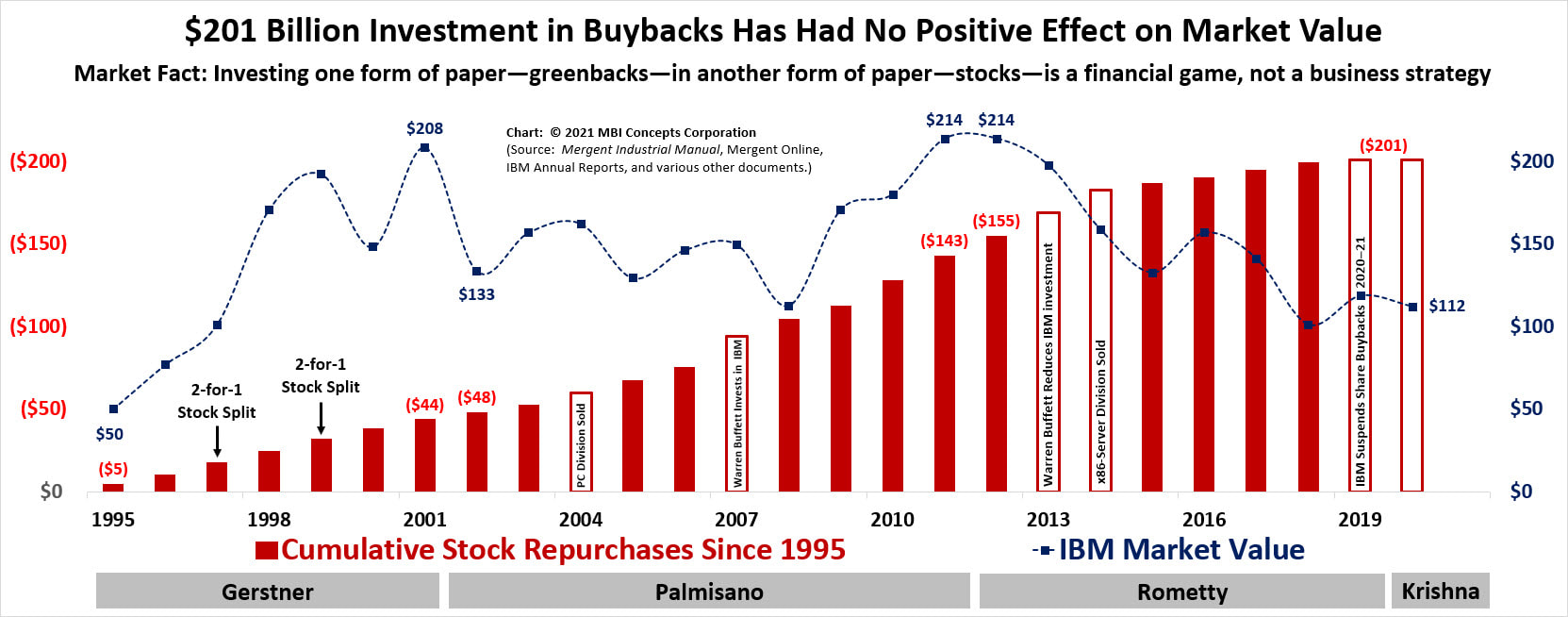

Was Warren Buffett right to sell his investment in IBM? From the chart below, the deterioration in market value after 2012 validates his decision to sell: an almost 50% drop in market value.

Share buybacks can not compensate for the market's lack of trust and confidence in a corporation's leadership.

Was Warren Buffett right to sell his investment in IBM? From the chart below, the deterioration in market value after 2012 validates his decision to sell: an almost 50% drop in market value.

Share buybacks can not compensate for the market's lack of trust and confidence in a corporation's leadership.

When Warren Buffett invested in IBM, he thought all he needed for his investment to be safe was castle walls and enduring moats, but the 20th Century IBM was always more than brick and mortar surrounded by deep ditches filled with water. Its walls and moats were defended by enthusiastic, engaged, and passionate stakeholders: customers, employees, shareholders, and their supportive societies.

Maybe, what Warren Buffet discovered after his investment is that the 21st Century IBM had long lost its "stakeholder magic" that had sustained it for so long through so many recessions and hard times. Its once great culture that maintained a sustainable stakeholder ecosystem of customers, employees, shareholders, and societies was dead.

Maybe, what Warren Buffet discovered after his investment is that the 21st Century IBM had long lost its "stakeholder magic" that had sustained it for so long through so many recessions and hard times. Its once great culture that maintained a sustainable stakeholder ecosystem of customers, employees, shareholders, and societies was dead.

|

Because of the corporation's on-going strategy of share buybacks the stakeholder ecosystem had been running on life support for almost two decades: since 1995. IBM wasn't buying shares opportunistically, it was practicing dollar-cost averaging. Wise for individuals, stupid for non-investment based corporations.

Warren Buffett's current belief in share buybacks is a fool's errand. There is no way to "do them right" because no chief executive officer is omniscient. I surely burst a few CEO bubbles out there with that statement. Warren's too? |

A history of IBM share buybacks

|

IBM Was More than Brick and Mortar, and Deep Ditches Filled with Water

When Warren Buffett invested in IBM, the investment community wanted to hear his down-to-earth wisdom. He believed that IBM would serve his interests as a long-term shareholder. He believed it had enduring moats surrounding an economic castle that would provide excellent returns while protecting his invested capital.

Watson Sr. built these moats, but his architecture included battlements manned by passionate, engaged, and enthusiastic stakeholders, because, to a competitor, a moat without defenders is just a pleasant water course; to keep his defenders vigilant, he practiced “profit for the customers, profit for the employees, and profit for the stockholders.” He extended this philosophy to include society when he said, “I don’t think any man in good health should retire. A man can retire from certain responsibilities, but he still has the responsibility to do something for others.”

There are examples in IBM’s long history of employees sacrificing for the sake of their shareholders; shareholders providing money to rescue the corporation; customers giving a trusted vendor time to deliver the right technology; a chief executive officer reducing his commissions to provide employee benefits; and society defending the principles upon which the business and the country were both based. During such times, open communication between stakeholders ensured that individuals understood the necessity of any temporary imbalance. IBM’s greatest chief executive officers initiated and controlled these discussions.

IBM’s true strength has always been in its investment community of man—consumer man, employee man, investor man and the society of man. These men and women stood guard on the battlements overlooking the corporation’s castle walls and moats: competitors beware!

Mr. Buffett should update his analogy, and probably—after reading this article—realize that . . .

. . . IBM's 21st Century battlements—because of stock buybacks—are poorly manned and womanned.

That was his mistake.

Watson Sr. built these moats, but his architecture included battlements manned by passionate, engaged, and enthusiastic stakeholders, because, to a competitor, a moat without defenders is just a pleasant water course; to keep his defenders vigilant, he practiced “profit for the customers, profit for the employees, and profit for the stockholders.” He extended this philosophy to include society when he said, “I don’t think any man in good health should retire. A man can retire from certain responsibilities, but he still has the responsibility to do something for others.”

There are examples in IBM’s long history of employees sacrificing for the sake of their shareholders; shareholders providing money to rescue the corporation; customers giving a trusted vendor time to deliver the right technology; a chief executive officer reducing his commissions to provide employee benefits; and society defending the principles upon which the business and the country were both based. During such times, open communication between stakeholders ensured that individuals understood the necessity of any temporary imbalance. IBM’s greatest chief executive officers initiated and controlled these discussions.

IBM’s true strength has always been in its investment community of man—consumer man, employee man, investor man and the society of man. These men and women stood guard on the battlements overlooking the corporation’s castle walls and moats: competitors beware!

Mr. Buffett should update his analogy, and probably—after reading this article—realize that . . .

. . . IBM's 21st Century battlements—because of stock buybacks—are poorly manned and womanned.

That was his mistake.

IBM Needs to Inspire Enthusiasm, Engagement, and Passion in its Stakeholders

IBM has lost, not just the enthusiasm of its employees, but the engagement and passion of its customers and shareholders. To find prosperity in its second century, IBM will need a new leader who will execute a business-first strategy that returns value to all the corporation’s stakeholders. If anyone needed a proof point that shareholders are disillusioned with IBM, Warren Buffett's experience should be proof enough.

How long will it take for analysts to realize that the same condition has existed for two decades for its employees?

Just look at IBM's sales and profit productivity numbers.

Warren should have started there.

Cheers,

- Peter E.

How long will it take for analysts to realize that the same condition has existed for two decades for its employees?

Just look at IBM's sales and profit productivity numbers.

Warren should have started there.

Cheers,

- Peter E.